I’m on the opposite side of common knowledge on this topic.

The argument for raising the least amount of capital needed is the gist of the lean funding paradigm.

It keeps the entrepreneur focused, instills creativity and grass roots street smarts. It forces iteration as the backbone of both market discovery and product development. Less is more is the net of it.

It also let’s the funder stay close to their investment, managing it by objectives in a sense, creating a perpetual funding cycle. You fund what the entrepreneur needs to get to the next stage of product or market proof.

It also means that the entrepreneur is always raising funds, always on a tight leash from the sources of capital, always on the stressful watch of cash flow.

The upside of this is the lean startup concept in a nutshell.

A brilliant mashup of ideas that the best startups use to harness the market itself as a catapult not as a chasm to cross.

It works well as an operational principal, but jumps the shark as a funding paradigm in most all instances.

My counter argument to why raising more, not less is often the smart move:

1. There has never been a plan or a budget that didn’t prove absolutely essential and invariably incorrect.

If you raise to a plan you will come up short. Plan for a smoother runway into what neither neither you nor anyone can imagine in detail.

2. Being cash poor drives poor decisions, keeps you in blinders to objectives and invariably stifles openness to market opportunities.

Focus is essential but having the creative freedom to consider change and opportunities is where great things happen.

3. Lean funding by definition puts the directional control in the hands of the funders not the entrepreneur.

It is equally incorrect to assume that the funder is always the source of wisdom and guidance and that entrepreneurs are children who will put their hands in the cookie jar and glut out if left to their own devices.

I believe that the best chances for success come from raising capital in a partnership paradigm. From people who are in it for the long haul and where a small group of them can provide guidance and operational expertise.

I also believe that winning happens because the entrepreneur just nails it.

When a leap into the void, often counter intuitive happens. When you push everything off the table, and rethink market connections in bold new strokes.

To do that you need a runway. You can’t be backed into the disrupting cycle of always raising funds and always heads down to a plan.

If you have to give away a bit more of the company to create that security, so be it.

You need guidance and oversight but as much, you need the freedom to move and follow you gut.

Cashflow is king. Make sure you have it.

There is a core anomaly between the ease of starting businesses today and the challenges around funding their growth and discovering market fit.

There is almost no friction to start something.

From tools to build with and pay as you go services to host on. From a plethora of early stage capital. And most important, a culture that has embraced entrepreneurship as a legitimate occupation.

It has never been easier to run with a hobby and see where it goes. Never been more possible that your tiny niche could become a global game changer.

The flip side is that while it certainly easier to start something it has become increasing difficult, and much more expensive, to find true market fit if not scale something to a success.

This has turned 360 degrees in my career.

When I first started raising capital it was a challenge to raise your initial funds. There was less funding available as the cascade of capital from successful startups was just beginning to trickle down. The idea of seed funding was in a neonatal state.

It’s much better now, just very different dynamics that have resorted the challenges.

The truth of course is that entrepreneurs are chasing the impossible.

Creating something new from an idea that could become a household brand is the work of the wonderfully obsessed and the unflinchingly unrealistic.

Then as now both.

To change how we as a society work, play, connect and share our lives brings amazing satisfaction—and sometimes wealth–but the odds of winning are not great.

The very framework that this happens against has changed dramatically.

The thresholds for market proof today are as ambiguous as they are stratospheric in most cases.

The attention spans of the consumer for trying new things has diminished to a nanosecond. Capital needed to get started is everywhere. The capital needed to grow it, more and more challenging to get.

You can simplify this to say that there is just so much noise that makes it harder to break through, the odds of success less and less, and the cost to get there increasing all the time.

That sounds to me like an excuse.

My takeaway after a career of doing this is that it has always been hard, damn near impossible actually.

I just see it as uniquely different today on three fronts:

The number of failed companies and emotionally exhausted entrepreneurs will dramatically increase.

This is the exhaust of the process and it will fall on the culture of today to mollify. We give lip service to the acceptability of failure but this is an emotional scar that foreshadowed the emergence of the entrepreneurial psychologist.

Those with capital to invest will become both more powerful and formative as they doll out funding in controlled pieces.

The upside is that from the best investor, the ability to mentor their investments increases. But the innate discordance between the portfolio view of an investor at the top of the funnel, and the single focus of an entrepreneur at the bottom will inevitably increase.

The net of these moving pieces is that the truly impossible is becoming possible to a broad population of entrepreneurs.

A founder with a big idea can truly believe that they can change the world. Not as an isolated instance but part of a culture, with strange analogs to the old Hollywood system that supports this.

We all see the obvious—the issues of creating more accessibility to this funnel to all economic classes, the recent awareness of the emotional toll of failure and the rising tide of wealth creating more for itself.

All this is true but whether it is easier or not, less expensive or not, doesn’t really matter.

What matters is that the impossible has become simply more possible.

That’s a truth that overshadows everything else and makes it worthwhile.

Words matter.

How we think about what we do, with what words, in many ways informs who we are and stylizes the businesses we create.

‘Lifestyle’ as a term is a case in point of this.

A word I rarely use to describe what a business does or its model, but just can’t seem to avoid when out looking for capital.

It’s an interesting conundrum, layered and ambiguous.

I keep wanting to reject the moniker but it sticks around in interesting ways.

Think of it this way.

There are ideas that change our world.

Reinventing how we educate our children, crowd sourcing innovation or rewiring transportation changes our very culture and stylizes how we live. When they succeed, they create enormous wealth that trickles down and reinvigorates the cities where they happen and the ecosystems they touch.

There is no question that what Uber has done for getting around, and what a rock star chef and restaurateur has done to an evening out over an astounding pizza with an approachable wine list are at different ends of the spectrum.

Culturally and financial obviously.

But life and business and intent are more grey, especially early on.

At inception, at a seed stage, what became AirBnB or Kickstarter and a drive to productize your grandmothers Kugel or your mother’s cookies are really starting at the same place.

Not so crazy as you may think.

Did they ever think Shake Shack was going to be a spun off as public company on its own? Or even Etsy?

We dance around this all the time.

We start projects today as we used to have hobbies.

We follow our passions and toil to find structures that platform them, communities that connect them, and invariably capital to support them.

I run into this divide often on the funding front—between concepts of tech and consumer, between future platforms and present satisfactions, between causes that are just damn right to do and things to make money.

What’s interesting is that while it is trivial to start anything today, it is more capital intensive to be successful and grow at any scale.

Sure, some things are by definition go big or go home.

Huge bets, huge wins by design. But even those, often at the first seed stage are so embryonic that it is unclear what they are about.

Some things are by definition, especially around hard goods, all about brand and figuring out how on a small scale they make business sense from a cash flow perspective, but at scale can be game changing home runs.

As a businessperson, I certainly understand that multiples matters and depending on your investment strategy, you determine how big a bet you need to take to make it pay back. As there are obviously markets that scale and cross sectors with more ease.

But this is breaking down quickly both in tech and out of it.

Within tech—or within an explosive network growth reality–the odds of any idea becoming the next Facebook is about the same as winning the lottery.

The belief and the possibility of creating something of value that can become an acquisition target and fit into one of the infrastructure giants that layer out our world—not as crazy.

Some investors, the most successful ones I know, approach this with a theory. Focusing on possibility more that the how of it.

For others, especially at seed stage, it’s just gut feel, looking for the cool and interesting. Invariably and counter intuitively, this group seems to force a model on the idea from the outset. An unnatural act in most circumstances.

On the consumer side, I’m discovering the same bias, the idea that disruption comes from a distribution strategy rather than a brand perspective.

Just not so, tech thinking on consumer realities is a bad mashup.

Are there more or less brands on the consumer side then on the tech side? Does selling pickles by definition create a limitation what with co-packing, franchising and geo distribution possibilities?

Sure—building something that captures human behavior where the users themselves are the content is more explosive than creating something that needs to get made and distributed.

But the maker revolution is cross sectors.

From consumer hard goods to green city guides to software that is a piece of the stack. The odds and the size of success are equal in my mind.

The power of a consumer brand surfacing above the massive din of social noise, an entity that has value equal if not more than many software solutions.

This to me is food for thought, not data for conclusions.

About the reality that capital is needed for the hard goods startup as much as the software company or a community platform.

The fact that solving problems is only a relevant piece of a plan for a very small, often a very limiting approach, to tackling a market.

The truth that bootstrapping is becoming more and more impossible, and I think often, the wrong way to start a business.

And mostly, the idea of defining and finding market traction that speaks to a future model, more and more aspirational if not stifling.

Where does lifestyle play into this?

Lifestyle in our mind’s eye, speaks to the idea dog friendly offices, sushi on Friday, and fully funded insurance plans.

Interestingly, I surfed over to a hot, well funded, huge-burn research start up job page this morning.

They are in SF, but the job page read like the ad copy for leasing a high end condo in the Meat Packing district in NY. All lifestyle and poise and to the P & L, lots of burn.

Light years away from most early startups and small companies living off credit cards and family support, scraping for the first deal to cover cash flow.

This is the take away thought about dangers of encapsulating ideas and possibilities before they are fully market formed.

Worth thinking about when we pitch for funds. Something for investors to ponder as well.

Few things are as pure as a transaction.

It’s the aggregate of factors affecting customer choice.

Where marketing, sales, customer want, brand value and UX mash together.

Where belief and timing intersect. Where trust meets the swipe of a credit card. Where a decision—a vote of commitment–is made.

Marketing generates scads of data. It’s inspired the science of analytics and measurement. We measure reach, build conjectures around engagement and social touch points. We even attempt to measure brand, the purest connection of belief to a market.

This data is really useful and essential to our job. It’s a tool of the trade but all of it is conjecture around behavior. None of it is not as revealing as what we learn from customers during the sales process.

In startups where you are in the business of selling things, putting a price on value, revenue is more a marketing data point than proof of a model. Especially early on.

More an indication of product market fit than anything else.

It is the truest KPI.

Think about your first $1M in revenue.

When you cross it. When you seriously believe that you are on the run rate towards it, it is pure magic. Emotive and primal and a damn epiphany.

It’s also a reality check and bellwether for investors. A gateway to a host of fundraising opportunities.

It’s certainly time to take the team to the bar.

Truth be told though, revenue, especially that first couple of million, has little to do with your future business model. Almost nothing to do with how efficient your model is today.

I’ll take the bet that 90% of the time how you are making money at the $1M mark will look completely different than at $20M, even $10M. The value you are selling at 20x today’s revenue may be the same but how you are delivering it won’t be.

Today you are muscling things into place. Creating consulting services before productizing the value.

You are touching flesh with each and every one who shows interest to find a connection. It’s romance that feels more solid than a fling.

It couldn’t however be more important, more indicative and more valuable.

What early revenue does is give you a glimpse of what your market could possibly look like.

You get the chance to see, maybe for the first time, what your brand looks like to the only individuals that matter, the customer and the superset of them, the market.

Marketers dream of visceral touch points with the market.

The best go out into the world and sell products to understand their customer behaviors at the point of sale. Online we fuss and obsess about every piece of data that implies a connection, a dynamic, or an understanding. But we are always one step removed from reality.

We desperately want to know what the customer thinks and are invariably stymied in that understanding.

The art of business is about creating an environment where sales is a natural process and where it is comfortable for a customer to discover and choose you.

How you do that is what defines success.

Marketing as a discipline builds the touch points and creates the environment for that to happen. Sales manages the timing of that choice, the understanding of how the thing you sell plays into the urgency of the customer to buy.

Revenue early on for startups is where this comes together.

I’ve been at that first $1M revenue mark a bunch of times.

Every time it happens it’s a wonder and invariably I can tell who bought what, when, how they felt about the purchase and where they found us.

This is information to die for.

This is the data to understand the connection between what you are selling and what the customer thinks they are buying. From that data you start to figure out how to scale what you have. How to price, deliver, expand the line and support it.

At my core I’m a brand builder who simply loves numbers, sales data especially.

I love them later on when they are the scorecard for company health and wealth. I love them early as they show you how to get there.

Building a business is all about making decisions.

Often from the gut, invariably through presupposition. Too frequently in the dark.

There is nothing like a transaction, like sales exposure, to make your assumptions and your decisions more concrete and more valuable.

That’s the real definition of a KPI.

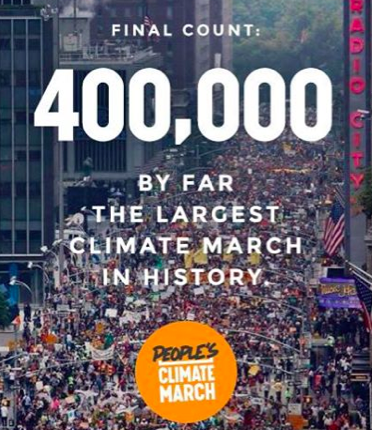

I simply couldn’t resist the urge to chronicle the Climate March, held this past Sunday in New York.

I simply couldn’t resist the urge to chronicle the Climate March, held this past Sunday in New York.

I was there and blown away by the sheer magnitude of people and spirit.

As a New Yorker living in the flood plain downtown, climate change is not an abstraction but reality, as two times out of the last three hurricane seasons, our building was evacuated and we were handed a personal warning sign of changes surely to come.

Of course, climate change touches everyone and everything not just us. From the rising level and temperature of the ocean, to how we produce nutrients to feed the world, to the rising alcohol levels in the wines we drink.

This march, even for NYC, with some 400,00 strong participating, was hyper symbolic simply by its density and size.

It was also a wondrous and large-scale mess from the crammed, uncontrollable mass of humanity overcrowding the uptown trains on a lazy Sunday morning to total bedlam at the intersection of 77th Street and Central Park West.

For myself, ever the pragmatic optimist, it was a graphic reinforcement of my personal belief that truly giving a shit about something, and sharing that belief, is a force that can change the world.

I was egged on to write this by a friend’s Facebook comments to my Instagram photos of the march. ‘Does it really matter?’ was her question punctuated with glass-half empty ennui and painted in inevitability of doom and gloom.

My response is undeniably—Yes!

It is the only thing that matters! Without caring nothing gets done.

Let’s be clear that what was united in this sea of chanting humanity at the march was the passion and collective acknowledgement of a real threat. That’s the key point.

Beyond that communion, it was a jumble of slogans, crazily diverse, many misguided, blaming our current state of the planet on everything from Wall Street to Obama, to industrialization to the decay of religion and ethics.

As diverse as the messages was the population. A melting pot of people, seniors and baby boomers aplenty, but way more teenagers acting out awareness, many costumed, dancing with childlike seriousness and pensive joy.

Granted that this march was more expression than platform, more celebration of unity than a coherent coalition or fund raising effort. Some of the secondary offshoots like Flood Wall Street, and Choose Life over Money seem counter productive if not misguided.

But—exultations at this level mollifies most everything else, even the practical, to some extent.

But—exultations at this level mollifies most everything else, even the practical, to some extent.

This was a gathering to show solidarity, to cheerlead the fact that people do care and are willing to do something about it.

I never found my group at the march and in my wandering about, two truths struck me, one from my heart and one absolutely from my head as a businessperson.

The largest cultural changes always comes from the heart of the people up, not from legislation and the government down.

This seems to play itself out time after time in my life.

People are the kernels of the largest changes, not government nor certainly institutions. People are in fact where businesses and government get their cue and permission to act.

Think back to the world you lived in the day after you graduated high school. My bet is the largest cultural changes you are living with today are the ones that you personally were part of making happen.

Civil rights, gender equality, the criminalization of bigotry and hate crimes, gay rights, sexual freedoms—even recycling and large scale composting–all started from people, from individual actions atomizing into groups and communities embracing trends that evolved society and eventually impacted government.

In my personal world, the change is really dramatic.

Post high school, no one was out of the closet, gender equality was an aspirational idea, with not even a hint of reality. Racial and religious intolerance was commonplace. Littering wasn’t even a concept and on the health front, lead was a prime ingredient in the paints used in every elementary school. Asbestos was wrapped around every plumbing pipe in NA.

All of these were taken on by the people and to varying degrees moved in the right direction against overwhelming odds. Fueled by the web of course and instantiating a new moral status of transparency and civil customer rights.

The world is hardly perfect but you are wearing blinders if you don’t see this as a better place and time. And even moreso if you don’t think the world’s population can’t tackle the massive issues affecting everyone—climate and equally of how to feed the world’s hungry without killing the planet itself.

I call bullshit on the doom and gloom crowd.

We shall prevail and not only will change happen it will happen in ways that drive our economy, not hurt it.

Saving the earth just may save the world’s economy

This is not a feeling, this is calculated hypothesis. Maybe optimistic but smacks of possibilities.

VCs are now talking about investing to do good. I applaud this but I also know they are following the money as well and investing smartly.

I believe the real money from capital investments over the next decades will come from AgTech more than tech, from logistics ingrained with sustainability and from leveraging science as truly the partner of computer and behavioral sciences.

I believe that projects around carbon footprints, growing more nutrient dense food per acre, water usage, power and land usage generally are ‘good’ as in the realm of stuff for the ‘common good’ but equally, they are where the smart money is going to be made.

The real reason I’m positive on the future is because good intentions and great business will come together here as a perfect wave.

That not only does the mass of people I followed down Central Park West have a heart to push and support change, but it is also the market for the products of change.

This group of 400,000 and the hundreds of millions they touch in their networks across the web, are both the spirit for change and the consumers who will support it with their choices of what to buy and what not.

This is a big deal. Product without markets fail. Markets chanting for products they can love, change the world we live in.

I also agree with Rob LeClerc, CEO of AgFunder, that AgTech as a category is the next major asset class in the capital markets.

If you can solve any one of thousands of critical agricultural supply chain opportunities, the market is already here.

Wrapping up

This was the best use of a Sunday afternoon I’ve done a while.

To say that people don’t care is simply not true. The march here and around the world proved that. People seriously are concerned and united around that concern.

To say that people don’t care is simply not true. The march here and around the world proved that. People seriously are concerned and united around that concern.

To think that world leaders can ignore this—I guess is possible, but not for long as the coming generations will be way less patient that we are. And they were out en mass at the march.

The real power here is that the people who were present were united in spirit and will create the market to support it.

From rose colored,peace-signed glasses on baby boomers to musings on AgTech economics—simply a great day.